The rising cost of a college degree can feel like an insurmountable barrier, but a high-quality education does not have to come with a lifetime of debt. The key to unlocking this future lies not in finding a single magic solution, but in strategically layering multiple forms of low-cost higher education financing. This approach requires early planning, diligent research, and a clear understanding of the financial landscape. By moving beyond high-interest private loans and focusing on grants, subsidized aid, and strategic personal choices, students and families can dramatically reduce the financial burden of a degree. This guide will walk you through a comprehensive framework for funding your education without compromising your financial future.

Building Your Foundation with Free Money

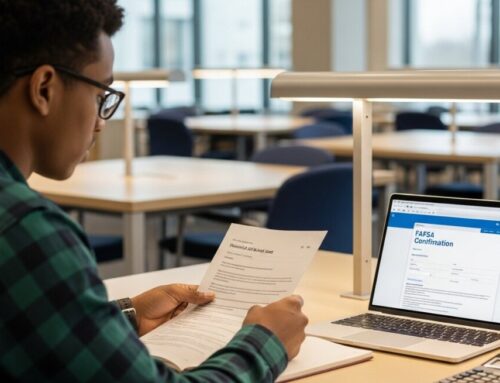

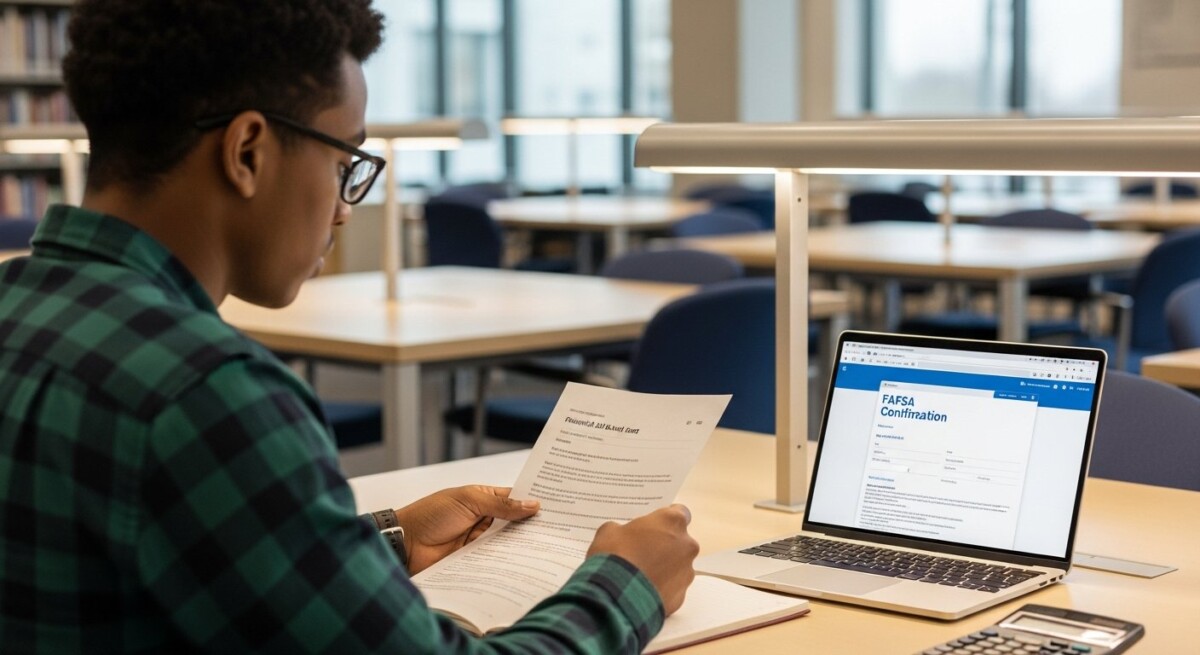

The cornerstone of any low-cost financing plan is maximizing funds that never need to be repaid. This category includes grants and scholarships, which are essentially gifts awarded based on financial need, academic merit, athletic talent, community service, or other specific criteria. The federal government is the largest source of grant money, primarily through the Pell Grant program for students with exceptional financial need. State governments also offer grants, often with residency requirements. Institutional grants from colleges and universities themselves are a critical piece of the puzzle, as schools use this aid to attract desirable students. The single most important step you can take is completing the Free Application for Federal Student Aid (FAFSA). This form is your gateway to federal grants, work-study, and loans, and is also used by most states and colleges to determine their own aid awards. Missing FAFSA deadlines is one of the biggest mistakes families make.

Beyond government and institutional aid, a vast universe of private scholarships exists. These are offered by corporations, non-profits, community organizations, and religious groups. While some are highly competitive, others are awarded based on unique hobbies, heritage, or career aspirations. The search requires effort but can pay significant dividends. A strategic approach involves starting early, staying organized, and applying broadly. Treat scholarship applications like a part-time job during your junior and senior years of high school. Remember, every dollar won in scholarships is a dollar you don’t have to borrow or earn later.

Federal Student Loans: The Safest Borrowing Option

When grants and scholarships do not cover the full cost, federal student loans should be your first borrowing choice. They are considered the bedrock of low-cost higher education financing due to their fixed interest rates, income-driven repayment plans, and borrower protections like deferment and forgiveness options. These loans are funded by the U.S. Department of Education. There are several types, each with specific terms. Direct Subsidized Loans are the most advantageous for undergraduate students with financial need. The government pays the interest on these loans while you are in school at least half-time and during grace and deferment periods. Direct Unsubsidized Loans are available to both undergraduate and graduate students regardless of financial need, but interest accrues from the moment the loan is disbursed.

For parents of dependent undergraduate students, Direct PLUS Loans are an option, though they have higher interest rates and fewer repayment protections than loans in the student’s name. A crucial aspect of managing federal loans is understanding the borrowing limits. For dependent undergraduates, annual limits range from $5,500 to $7,500 for the first year, with aggregate limits capping total borrowing. This structure is designed to prevent over-borrowing but often means federal loans alone may not cover the entire cost of attendance at expensive institutions. This is where strategic gap-filling becomes essential. For a deeper dive into the nuances of each federal loan type and application strategy, our guide on navigating affordable higher education financing options provides a detailed breakdown.

Strategic Cost Reduction Before You Borrow

Lowering the total price tag of your degree is the most effective way to reduce borrowing needs. This involves making deliberate choices about where and how you pursue your education. One of the most powerful strategies is starting your degree at a community college. Completing general education requirements at a local two-year institution before transferring to a four-year university can save tens of thousands of dollars in tuition and fees. Ensure you work closely with advisors at both schools to guarantee credits transfer seamlessly.

Choosing an in-state public university over an out-of-state or private institution almost always results in significant savings. Furthermore, accelerated degree programs, such as taking Advanced Placement (AP) exams in high school or overloading credits during college semesters, can allow you to graduate a semester or even a year early, slashing the cost of tuition, fees, and living expenses. Living off-campus with roommates, buying used textbooks, and utilizing student discounts for software and services are all practical ways to minimize day-to-day costs. The goal is to scrutinize every expense associated with the college experience and seek a lower-cost alternative without sacrificing academic quality.

Exploring Work-Based Funding Options

Earning money while in school directly offsets the amount you need to borrow. The Federal Work-Study program provides part-time jobs for undergraduate and graduate students with financial need, allowing them to earn money to help pay education expenses. These jobs are often on-campus and designed to accommodate academic schedules. Even if you do not qualify for work-study, seeking part-time employment, a paid internship in your field, or a cooperative education (co-op) position can provide invaluable income and professional experience. Some employers, including major corporations and retail chains, offer tuition assistance or reimbursement programs for their part-time or full-time employees. Working for such a company can be a strategic way to fund your education over time.

Responsible Use of Private and Alternative Financing

After exhausting all free aid, federal loans, and cost-cutting measures, a gap may still remain. This is where private student loans from banks, credit unions, and online lenders enter the picture. It is critical to approach private loans with caution. They lack the flexible repayment and forgiveness options of federal loans and often have variable interest rates that can increase over time. However, for borrowers with excellent credit (or a co-signer who has it), they can sometimes offer competitive rates. If you must consider private loans, follow these steps to secure the best possible terms:

- Exhaust all federal loan options first. Always accept your full federal loan eligibility before looking at private loans.

- Shop around aggressively. Get rate quotes from multiple lenders, including local credit unions which may offer favorable terms to members.

- Compare the full picture. Look beyond the advertised interest rate. Consider fees, repayment term options, and whether the rate is fixed or variable.

- Understand the co-signer requirement. Most students will need a creditworthy co-signer. A co-signer is equally responsible for the debt, and the loan will appear on both credit reports.

- Borrow only what is absolutely necessary. Use a detailed budget to calculate your exact gap, and resist the temptation to take out extra for lifestyle expenses.

Alternatives like home equity lines of credit (HELOCs) or borrowing from retirement accounts are generally not recommended for funding education due to the risks involved, such as putting your home or retirement security at stake.

Long-Term Financial Planning and Repayment Strategy

The journey toward low-cost financing does not end at graduation, it extends into a smart repayment plan. For federal loan borrowers, selecting the right repayment plan is paramount. The Standard 10-Year Plan is the default, but Income-Driven Repayment (IDR) plans like SAVE, PAYE, and IBR can cap your monthly payment at a percentage of your discretionary income, making payments more manageable, especially in early career years. Under IDR plans, any remaining balance may be forgiven after 20 or 25 years of qualifying payments. Public Service Loan Forgiveness (PSLF) is another powerful program that forgives the remaining balance on Direct Loans after 120 qualifying monthly payments under a qualifying repayment plan while working full-time for a qualifying employer, such as a government or non-profit organization.

Developing a post-graduation budget that prioritizes loan payments is essential. Even making small interest payments on unsubsidized loans while still in school can prevent interest from capitalizing and adding to your principal balance. Automating payments can often secure a small interest rate discount from your servicer. The overarching principle is to view your student loans as an investment that requires active management, not a passive bill. A proactive approach to repayment is the final, critical step in ensuring your education financing remains low-cost over its entire lifecycle.

Frequently Asked Questions

What is the biggest mistake families make when seeking financial aid?

The most common and costly mistake is not filing the FAFSA at all, or filing it late. Many families assume they won’t qualify for aid due to their income level, but the FAFSA is required for federal loans and most institutional aid, regardless of need. Missing state and college deadlines can also mean leaving thousands of dollars in aid on the table.

Are scholarships only for straight-A students or star athletes?

Absolutely not. While many scholarships reward academic or athletic excellence, thousands more are based on community service, leadership, specific career interests, heritage, hobbies, employer affiliations, or even essay contests. A diligent search can uncover opportunities for a wide range of students.

Should I choose a cheaper school over a more prestigious one?

This is a complex decision that balances cost, career goals, and program quality. In many fields, the specific skills and internships you secure matter more than the school’s name. For pre-professional tracks like engineering or nursing, ensure the program is properly accredited. Often, the best value is a solid in-state public university or a community college transfer pathway.

Is it ever a good idea to use a credit card to pay for college costs?

Using credit cards for direct tuition payments is almost always a bad idea due to extremely high interest rates. They should only be considered for emergency expenses if no other option exists, and the balance should be paid off immediately. Some families use cards strategically to earn rewards points for books or supplies, but only if they pay the statement balance in full every month to avoid interest.

How can I improve my chances of getting a low-interest private loan?

Building or improving your credit score is key. This means paying all bills on time, keeping credit card balances low, and avoiding new debt. If your credit is limited, having a co-signer with a strong credit history and stable income is the most effective way to secure a favorable rate. Always compare offers from multiple lenders.

Financing a college degree is a significant undertaking, but it does not have to lead to a paralyzing debt load. By adopting a strategic, layered approach, you can construct a financial plan that leverages free aid, utilizes low-cost federal loans, minimizes expenses through smart choices, and borrows privately only as a last resort with careful terms. This proactive and informed path to low-cost higher education financing empowers you to invest in your future without mortgaging it, turning the dream of a degree into a sustainable reality.

{kind=link}

{kind=link}

{kind=link}